The $250 Billion “Frenemy” Pact: Why the Microsoft-OpenAI Marriage Is Over (And the War Has Begun)

TL;DR

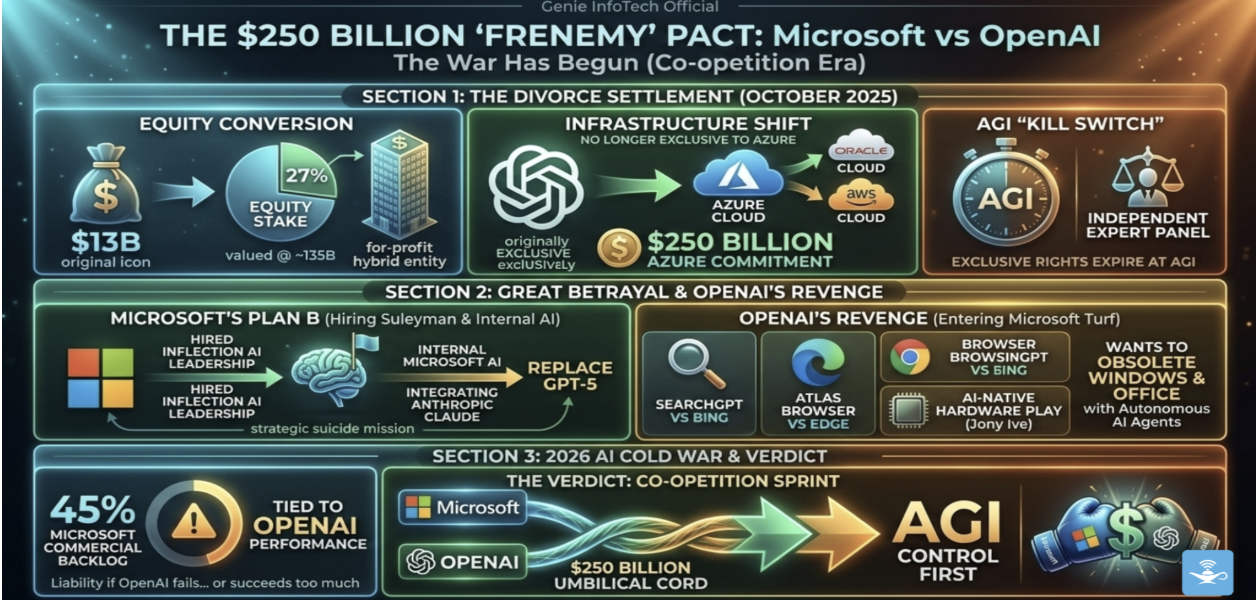

- Microsoft invested $13 billion in OpenAI, got 27% equity worth ~$135 billion and is now building its own frontier AI models.

- OpenAI signed a $300 billion Oracle deal, is building products that compete with GitHub Copilot, and plans to cut Microsoft’s revenue share from 49% to 8% by 2030.

- Microsoft AI chief Mustafa Suleyman confirmed in February 2026 that the company is pursuing “true AI self-sufficiency.”

- For any company building on top of these platforms, multi-model architecture is no longer optional it’s survival.

For five years, the alliance between Microsoft and OpenAI was the most formidable force in technology. It was a simple trade: Microsoft provided the massive supercomputing power (Azure) and billions of dollars, while OpenAI provided the “brains” (GPT-4) that powered Microsoft’s global resurgence.

Copilot became an enterprise juggernaut. Bing became something people actually tried. Azure became the default cloud for AI workloads.

Then, in 2026, the whole thing fell apart not with a dramatic announcement, but through a series of moves that made the breakup inevitable long before either side said the word out loud.

This article breaks down exactly what happened, why it happened, and what it means for anyone building software today.

The Deal That Started It All

Microsoft’s first investment in OpenAI came in 2019 $1 billion for exclusive cloud access and a front-row seat to whatever OpenAI built next. At the time, OpenAI was still a nonprofit research lab with big ambitions and no revenue.

By January 2023, right after ChatGPT went viral, Microsoft poured in another $10 billion. The total commitment eventually crossed $13 billion. In exchange, Microsoft got exclusive cloud rights, access to all OpenAI models, and a share of OpenAI’s future profits reportedly up to 49%.

There was one unusual clause buried in the agreement: if OpenAI ever achieved artificial general intelligence (AGI), as determined by OpenAI’s own board, Microsoft’s commercial rights would be terminated.

At the time, AGI felt theoretical. Nobody expected that clause to matter anytime soon.

It mattered.

The Cracks: A Timeline

November 2023-The Board Fires Altman

OpenAI’s board removed Sam Altman as CEO without warning. Microsoft which had billions riding on the partnership wasn’t consulted. Within 48 hours, Microsoft offered to hire Altman and his entire team. The crisis resolved when Altman returned, but the message was clear: Microsoft had staked its AI future on a company where a four-person board could blow everything up overnight.

Internally, Microsoft started hedging.

January 2025-OpenAI Restructures

OpenAI and Microsoft agreed to let OpenAI restructure its corporate setup, giving OpenAI more independence over its operations and compute resources. The same month, OpenAI launched the $500 billion Stargate Project with SoftBank and Oracle, not Microsoft to build new AI infrastructure across the US.

OpenAI’s single largest infrastructure bet didn’t include its biggest investor.

April 2025-Microsoft Pulls Back

Microsoft announced it would no longer support ChatGPT training directly, as OpenAI gained financial autonomy following a $40 billion SoftBank investment.

June 2025-The Oracle Deal

OpenAI signed a $300 billion agreement with Oracle for 4.5 gigawatts of compute capacity actively diversifying away from Azure. For context, this single deal was larger than many countries’ annual technology budgets.

October 2025-The Restructuring Agreement

After nearly a year of tense negotiations, both sides finalized the restructuring deal. The key terms tell the real story:

What Microsoft got:

- 27% equity in OpenAI (~$135 billion at current valuation)

- IP rights and Azure API exclusivity through 2032

- AGI determinations now reviewed by an independent panel (no longer OpenAI’s board alone)

What Microsoft lost:

- Exclusive cloud provider status OpenAI can now use other providers freely

- Revenue share drops from 49% to a planned 8% by 2030

- The ability to block OpenAI from competing directly

Going from 49 cents of every dollar to a planned 8 cents isn’t a renegotiation. It’s a severing.

February 2026-Microsoft Declares Independence

Mustafa Suleyman, Microsoft’s AI chief and DeepMind co-founder, made it official in a Financial Times interview:

“We have to develop our own foundation models, which are at the absolute frontier, with gigawatt-scale compute and some of the very best AI training teams in the world.”

He called it “true AI self-sufficiency.” Microsoft confirmed it would release its own frontier-grade MAI models sometime in 2026 while also investing in Anthropic and adding Claude to Azure alongside OpenAI models.

Microsoft comms chief Frank Shaw tried to soften the message: “We are in a multi-model world. OpenAI has a huge role for us AND we are building frontier models for specific things.”

The “AND” is doing a lot of heavy lifting in that sentence.

March 2026-Direct Competition

Reports emerged that OpenAI is building a product that directly competes with GitHub Microsoft’s $7.5 billion developer platform. OpenAI’s Codex had evolved from a code-generation tool into an agentic software development platform that overlaps directly with GitHub Copilot.

Meanwhile, Sam Altman had been personally pitching 300+ enterprise executives to switch from Microsoft Copilot to OpenAI’s direct offerings. His pitch, essentially: work with the company that built the AI, not the middleman. For every startup building a mobile app or web product with AI features, this power struggle directly affects which APIs stay stable, which get repriced, and which disappear entirely.

Why the Marriage Failed

Three fundamental tensions made this breakup inevitable.

1. OpenAI Outgrew the Deal

When you go from a nonprofit research lab to a platform with 900 million weekly active users processing 2.5 billion queries per day, the economics change. OpenAI’s revenue scaled from $2 billion (2023) to $6 billion (2024) to $20 billion (2025). No enterprise software company in history has grown revenue that fast Salesforce took 20 years to reach the same number.

At that scale, giving up 49% of revenue to a cloud provider feels less like a partnership and more like a tax.

2. Microsoft Couldn’t Control the Risk

The November 2023 board crisis revealed a structural problem: Microsoft had built Copilot, its most important product line, on top of a company it didn’t control. The AGI clause gave OpenAI theoretical power to cut Microsoft off entirely. That’s unacceptable for a $3 trillion company answering to shareholders.

Microsoft’s move toward self-sufficiency isn’t about ego. It’s risk management at scale.

3. Both Companies Now Want the Same Customers

OpenAI launched ChatGPT Enterprise, targeting the exact same corporate buyers Microsoft was selling Copilot to. OpenAI started building developer tools that compete with GitHub. Microsoft started integrating Claude and other models to reduce OpenAI dependence.

When your partner starts going after your customers, the partnership is over regardless of what the contract says.

The $285 Billion Side Effect

The breakup isn’t happening in a vacuum. When Anthropic launched Claude Cowork in January 2026, software stocks crashed $285 billion in a single week. Investors are pricing in a world where AI agents don’t just assist work they replace entire categories of enterprise software.

Microsoft building its own models. OpenAI going direct to enterprise. Anthropic eating the productivity software market. Google pushing Gemini across everything.

The AI landscape went from “one dominant partnership” to a multi-front war in less than 12 months.

What This Means for Companies Building Software

This is where the analysis gets practical, and where it matters most for anyone evaluating technology partners, choosing AI providers, or architecting products in 2026.

Multi-Model Architecture Is Now Mandatory

Any product built exclusively on a single AI provider is carrying unnecessary risk. The provider landscape is shifting quarter by quarter. What works today might be deprecated, repriced, or outperformed tomorrow.

The smart approach: build an abstraction layer between your application logic and the AI provider. Switching from OpenAI to Claude or Gemini should be a configuration change, not a rewrite. Whether you’re building a SaaS platform or an internal enterprise tool, this adds 1–2 weeks of upfront development time but eliminates months of potential migration work later.

Azure Is Becoming More Useful, Not Less

This might sound counterintuitive, but Microsoft’s breakup with OpenAI actually makes Azure a better platform. Instead of being locked to one model provider, Azure is becoming a genuine multi-model marketplace offering OpenAI, Claude (Anthropic), Llama (Meta), Mistral, and Microsoft’s own upcoming MAI models. For enterprises already on Azure, this is an advantage.

Watch the Cash

OpenAI has zero dollars in profit. Annual expenditures are approaching $89 billion. The company requires constant capital injections from SoftBank, Microsoft, and others to stay operational. An IPO is planned, but the path from here to profitability is unclear.

This doesn’t mean OpenAI will collapse. It means that building critical business infrastructure on a company with this financial profile requires contingency planning.

The Vendor Lock-In Lesson

The Microsoft-OpenAI breakup is the most expensive lesson in vendor lock-in the tech industry has ever seen. Microsoft built its most important products on top of a partner it couldn’t control. OpenAI built its infrastructure on a provider it wanted to leave.

Both sides are now spending billions to undo decisions they made when the relationship felt permanent.

For any company building enterprise software or evaluating technology partnerships in 2026: if the partnership can’t survive a strategic disagreement, the architecture shouldn’t depend on it.

What Happens Next

Mid-2026: Microsoft releases its first frontier MAI model. It probably won’t beat GPT-5 on benchmarks, but it only needs to be good enough for Copilot and Microsoft 365 which is all that matters for their enterprise strategy.

Late 2026: OpenAI pursues its IPO at a $500 billion+ valuation. The cash burn question will dominate investor discussions. Revenue growth is extraordinary, but profitability remains distant.

2027: We enter a true multi-model world. Enterprises will routinely use 3–5 different AI providers simultaneously, optimized for different tasks. The “which AI do you use?” question will sound as dated as “which database do you use?” the answer will be “several, depending on what we’re doing.” Companies that lack in-house AI expertise will increasingly rely on dedicated development teams that can navigate this complexity.

The wildcard: If OpenAI’s financial situation deteriorates before the IPO completes, or if Microsoft’s MAI models underperform, the entire landscape reshuffles again. In AI, 18 months is a lifetime.

The Bottom Line

The Microsoft-OpenAI partnership changed computing forever. It proved that AI could be a mainstream product, not just a research project. It created the Copilot economy. It forced Google, Amazon, and every enterprise software company to rethink their entire strategy.

But the partnership also proved something else: in technology, no alliance survives the point where both sides want to be the platform.

Microsoft wants to own the AI stack. OpenAI wants to own the AI customer. Those two goals are incompatible. Everything that’s happened since the Oracle deals, the self-sufficiency declarations, the competitive product launches is just the inevitable conclusion playing out in real time.

For anyone building software in 2026, the takeaway is straightforward: architect for a world where today’s dominant AI provider might be tomorrow’s second option. Build flexible. Build multi-model. Build for change.

That’s the approach we’ve taken on every project from logistics platforms to fintech apps to SaaS products and it’s the only approach that makes sense when the ground keeps shifting.

Because in the AI industry right now, the only thing you can count on is that the landscape will look completely different in 18 months.

Frequently Asked Questions

Why did Microsoft and OpenAI break up? OpenAI outgrew the revenue-sharing structure, Microsoft couldn’t control governance risk after the November 2023 board crisis, and both companies began directly competing for enterprise customers. In February 2026, Microsoft AI chief Mustafa Suleyman confirmed the company is pursuing “true AI self-sufficiency” by building its own frontier models.

Does Microsoft still have access to OpenAI models? Yes. Under the October 2025 restructuring deal, Microsoft retains IP rights and Azure API exclusivity through 2032, including any models that reach AGI now verified by an independent panel rather than OpenAI’s board.

How much did Microsoft invest in OpenAI? Microsoft invested a total of approximately $13 billion in OpenAI between 2019 and 2023. Under the October 2025 restructuring, Microsoft received a 27% equity stake worth approximately $135 billion at current valuation.

What is the Stargate Project? A $500 billion AI infrastructure initiative launched by OpenAI with SoftBank and Oracle in January 2025 to build compute capacity across the United States. Microsoft was not included in the project.

Is OpenAI profitable? No. As of early 2026, OpenAI has zero dollars in profit and annual expenditures approaching $89 billion. The company relies on continuous capital injections from investors including SoftBank, Microsoft, and others. An IPO is planned but the path to profitability remains unclear.

Should companies still build on Azure OpenAI APIs? Azure remains a viable platform through 2032. However, Microsoft is actively adding Claude (Anthropic), Llama (Meta), Mistral, and its own upcoming MAI models to Azure making it a multi-model marketplace. Building a provider-agnostic abstraction layer is now considered essential to avoid vendor lock-in.

What is multi-model AI architecture? Multi-model architecture means building an abstraction layer between your application logic and AI providers, allowing you to switch between OpenAI, Claude, Gemini, or other models through configuration changes rather than code rewrites. This protects against vendor lock-in, pricing changes, and service disruptions.

QA Engineer

A writer and strategist at Genie InfoTech, a software development company in Dhaka, Bangladesh.

Comments

Read Next

The Success Tax: An Engineering Post-Mortem of the Claude 2026 Global Outage

On Monday, March 2, 2026, the artificial intelligence landscape experienced a “tectonic shift” that culminated in a global infrastructure failure.

.NET Core vs Laravel in 2026: We Use Both, Here’s How We Decide

We build on both .NET Core and Laravel in production. Our logistics platform (2,000+ stops/day) runs on .NET. Our invoicing product runs on Laravel. This isn't about which is better it's the decision framework we actually use, with real benchmarks, real costs, and when to pick which.

The Axios Hack of 2026: How a Trusted npm Library Quietly Became a Backdoor Into Thousands of Apps

A stolen npm token. A hidden post-install script. 45 million weekly downloads turned into an attack surface. The Axios supply chain hack of March 2026 was invisible, precise, and terrifying. We break down the 6-step attack chain, the blast radius, and what every dev team should change today.